No. You could not make this up.

Email 1

Email 1. Sent on 9th July 2026

———- Forwarded message ———

From: Paul Cardin

Date: Thu, 9 Jul 2026 at 08:07

Subject: corrected version – FORMAL NOTICE OF INSPECTION: STATUTORY REQUEST FOR ACCOUNTS AND SUPPORTING RECORDS

To: danielkirwan@wirral.gov.uk danielkirwan@wirral.gov.uk, matthewbennett@wirral.gov.uk, Fin_publicinspection@wirral.gov.uk

Cc: Basnett, Paula (Councillor) paulabasnett@wirral.gov.uk

For the attention of the Section 151 Officer / Executive Director of Finance / Shaun Allen

Dear Section 151 Officer / Executive Director of Finance / Shaun Allen,

I am writing to explicitly set out my statutory inspection request.

To ensure a proportionate approach that places no unnecessary administrative burden on your team, please consider my targeted request set out below.

This request focuses exclusively on core accounting ledgers and active contracts, removing any need for broad manual corporate searches.

Please process the following request under Section 26 of the Local Audit and Accountability Act 2014:

As a local government elector for the Metropolitan Borough of Wirral, I am writing to exercise my explicit statutory right under Section 26 of the Local Audit and Accountability Act 2014 to inspect the Council’s accounting records and related documents during the current 30-working-day public rights window.

To ensure this request is strictly proportionate, manageable, and legally compliant with the definitions upheld in Moss v Royal Borough of Kingston upon Thames (2021), I am limiting my inspection exclusively to financial ledger records and active contracts related to specific asset transactions.

Please provide digital access to, or an inspection appointment for, the following specific items:

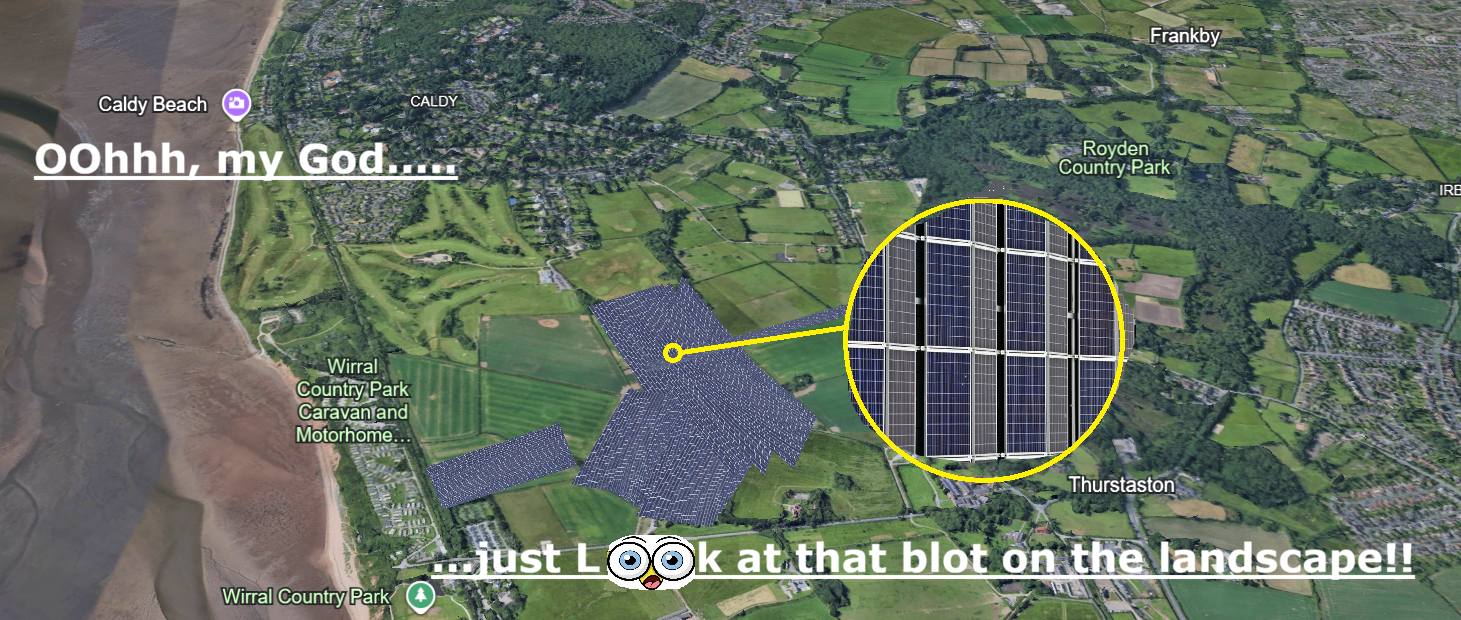

The Income Ledgers: All ledger entries recording rental income, wayleave fees, or site-share revenue received by Wirral Council from telecommunications operators during the 2025/2026 financial year.

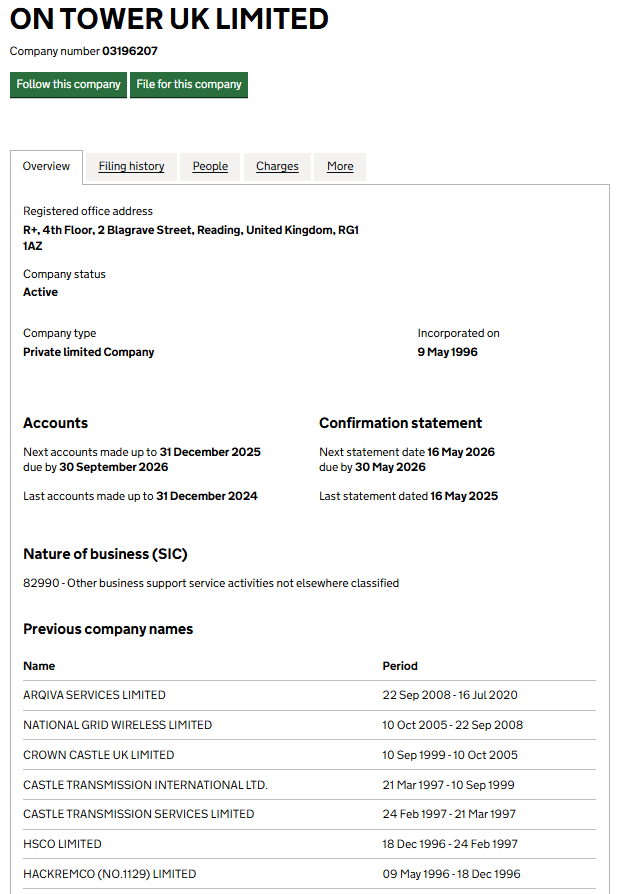

The Associated Contracts: Copies of the underlying lease agreements, pavement permits, or wayleave contracts corresponding directly to those 2025/2026 telecommunications income streams (protected as inspectable “contracts” and “deeds” under Section 26(1) of the Act).

The Insurance Expenditure Records: The Council’s active Corporate Public Liability Insurance policy schedule for the 2025/2026 financial year, alongside the specific ledger receipt/voucher confirming the premium payment made to the insurer.

As these requests pertain directly to financial transaction ledgers, active revenue contracts, and expenditure vouchers, they sit firmly within the statutory scope of Section 26. They do not require broad manual narrative searches, thereby removing any grounds for rejection based on administrative burden.

Please confirm within the next 48 hours when these files will be made available for my inspection so that I may review them prior to the close of the statutory window.

I look forward to your swift response with the digital files and inspection dates,

Yours faithfully,

Paul Cardin

Wallasey

Merseyside

Response 1

The following inadequate response arrived four days later from officer Shaun Allen on 13th July 2026:

———- Forwarded message ———

From: FIN_PublicInspection, <Fin_publicinspection@wirral.gov.uk>

Date: Mon, 13 Jul 2026 at 09:51

Subject: RE: *corrected version* – FORMAL NOTICE OF INSPECTION: STATUTORY REQUEST FOR ACCOUNTS AND SUPPORTING RECORDS

To: Paul Cardin

Good morning, Mr Cardin,

Thank you for your enquiry. We will look into your request, it will take some time to investigate and collate, but we will aim to get the details to you by the end of July. I will advise if there is any delay beyond that date.

Many thanks,

Shaun

Email 2

Email 2. Sent on 13th July 2026

———- Forwarded message ———

From: Paul Cardin

Date: Mon, 13 Jul 2026 at 21:02

Subject: Public Notice of Inspection

To: Fin_publicinspection@wirral.gov.uk

Cc: matthewbennett@wirral.gov.uk, danielkirwan@wirral.gov.uk danielkirwan@wirral.gov.uk, Hall, Brenda (Councillor) brendahall@wirral.gov.uk, Shaw, Vicki L. (Wallasey Town Hall) vickishaw@wirral.gov.uk, Basnett, Paula (Councillor) paulabasnett@wirral.gov.uk, sarah.l.ironmonger@uk.gt.com

Dear Mr Allen,

Thank you for your response, however, aiming to respond to me at a later date is inadequate.

While I appreciate you looking into this matter, your proposal to delay production of these records until the end of July is legally unacceptable. It would effectively deny me my statutory rights.

The Local Audit and Accountability Act 2014 mandates that the inspection of accounting records must take place during the strict 30-working-day public rights window. Were you to defer my access until after this window has closed it would prevent me from exercising my right to raise formal objections with the local auditor.

Given the severe compliance risks associated with blocking or delaying statutory access, I have copied key senior officers and oversight figures into this correspondence for the reasons set out below:

• The External Auditor: Copied so they are immediately aware that the Council’s proposed timeline prevents a local elector from reviewing records within the lawful inspection window, directly disrupting the statutory audit process.

• The Chief Executive (Head of Paid Service): Copied to ensure executive visibility over an operational delay that exposes the local authority to legal non-compliance.

• The Monitoring Officer: Copied in fulfillment of their statutory duty under Section 5 of the Local Government and Housing Act 1989 to investigate and halt any acts or omissions by the Council that risk breaking the law.

• The Chair of the Audit and Risk Management Committee: Copied to ensure robust political and governance oversight regarding the obstruction of statutory transparency measures.

• The Leader of the Council: Copied so that the political leadership is fully apprised of executive actions that undermine public accountability.

As noted in my initial request, the scope of this inquiry has been intentionally restricted to transaction ledgers, specific active contracts, and an insurance voucher. As established in Moss v Royal Borough of Kingston upon Thames (2021), administrative convenience or internal resource pressure cannot be used to defeat a statutory right of inspection.

Please re-evaluate this timeline immediately to ensure Wirral Council remains compliant with its statutory duties.

I require written confirmation within the next 24 hours of either a digital release date or an inspection appointment that falls safely within the current public rights window.

In year 2015/16 I successfully halted and froze Wirral Council’s accounts in the area of controversial £multi-million LOBO loans. Given my personal history, your current response could very well be interpreted as unfair, targeted discrimination,

Yours sincerely,

Paul Cardin

about.me/paul.cardin

Email 3

Email 3. Sent to Grant Thornton’s auditor on 19th July 2026

———- Forwarded message ———

From: Paul Cardin

Date: Sun, 19 Jul 2026 at 08:22

Subject: Obstruction and delay over statutory accounts inspection

To: sarah.l.ironmonger@uk.gt.com

Cc: matthewbennett@wirral.gov.uk, Basnett, Paula (Councillor) paulabasnett@wirral.gov.uk

Dear Ms Ironmonger,

I am writing to you in your capacity as the appointed external auditor for Wirral Metropolitan Borough Council under the Local Audit and Accountability Act 2014.

In the event I have the wrong person, please pass this message urgently to the Grant Thornton accountant dealing with Wirral Council.

I am a local elector for the Wirral area. I am writing to formally report that Wirral Council is currently obstructing and delaying my statutory right to inspect its accounts and accounting documents under Section 26 of the Act.

The Council published its Public Notice of Inspection for the 2025/26 accounts, establishing a strict 30-working-day window for public scrutiny. On 9th July 2026 (see attached email 1), which falls strictly within this active window, I submitted a formal request to the Council to inspect specific background documents, including:

The Income Ledgers: All ledger entries recording rental income, wayleave fees, or site-share revenue received by Wirral Council from telecommunications operators during the 2025/2026 financial year.The Associated Contracts: Copies of the underlying lease agreements, pavement permits, or wayleave contracts corresponding directly to those 2025/2026 telecommunications income streams (protected as inspectable "contracts" and "deeds" under Section 26(1) of the Act).The Insurance Expenditure Records: The Council's active Corporate Public Liability Insurance policy schedule for the 2025/2026 financial year, alongside the specific ledger receipt/voucher confirming the premium payment made to the insurer.

To date, the Council has failed to provide access, offering only delays and vague timelines.

I have emailed the Council on 9th July 2026 (see attached email 1) and 13th July 2026 (see attached email 2) in an attempt to obtain these documents yet I am faced with delays or non responses (see below).

As the National Audit Office (NAO) guidance clarifies, this 30-day window is a rigid statutory timeframe that you, as the auditor, have no legal power to extend. By delaying their response, Wirral Council is effectively running down the clock on my inspection period. This prevents me from identifying potential errors, checking value-for-money arrangements, or exercising my subsequent right under Section 27 to frame precise questions or lodge formal objections with you.

Given the severe financial stress and governance concerns highlighted in your recent Auditor’s Annual Report for Wirral Council, transparency during this public rights window is more critical than ever.

I urgently request that your audit team contacts the Director of Finance (S151 Officer) at Wirral Council to remind them of their mandatory duties under the Accounts and Audit Regulations. The Council must be instructed to provide immediate, unhindered access to the requested materials before my statutory window expires.

I have attached a full log of my correspondence with the Council’s finance team (emails 1 and 2) for your immediate review.

I have also copied this email to the council leader and CEO in an attempt to encourage them to resolve the errant conduct of junior officers under their charge,

Yours sincerely,

Paul Cardin

about.me/paul.cardin

Despite my request for a response by 14th July, six further days have elapsed with no response. I’ve notified the auditor, copied the above prompting email to Wirral Council today – 19th July – and I’m still no further forward. That’s a total of 10 days lost…

This process has now taken an unexpected turn…

Response 2

[[[[An email was received this morning (Monday 20th July) from Michael Green of Grant Thornton containing a useful attachment.

Michael Green has taken over from Sarah Ironmonger as Wirral Council auditor. His email also contained the following security caveat …

“Commercial in Confidence”.

This could appear on every one of his emails, OR it may have been done to prevent me exercising a blogger’s customary freedom of speech.

I’ve made enquiries via email and hopefully, the full email will be published here soon.]]]]

An important quote from Michael Green’s email:

“…delays you feel you are experiencing…”

I beg to differ, but as stated previously, I could have been granted access to these accounts on 10th July. It’s now 20th July. That’s an obvious, factual, on the record delay of 10 days.

Ultimately, if access is blocked by the council, I’m not sure who to turn to?!

The Citizen’s Advice Bureau is a dead end, and consulting my own solicitor would cost lots of money; money I don’t have access to.

Lack of funds put paid to my last qualifying objection to Wirral Council’s accounts.

Also, it looks like electors can only object to the accounts after inspecting them. And I don’t think that will be permitted to happen. That’s my gut feeling here after blogging on abusive Wirral Council for the last 15 years.

Email 4

Email 4. Sent on 20th July 2026

———- Forwarded message ———

From: Paul Cardin

Date: Mon, 20 Jul 2026 at 21:51

Subject: Re: Re – Obstruction and delay over statutory accounts inspection

To: Michael Green <Michael.Green@uk.gt.com>

Subject: Official Submission of Audit Evidence: Obstruction of Electors’ Rights – Wirral MBC Audit

Dear Mr. Green,

Thank you for your email and for confirming your role as the Engagement Lead for the Wirral MBC audit.

While you state this is not a matter you can help with, I am formally submitting this tracking of the Council’s silence as direct audit evidence. A council obstructing an elector’s statutory inspection rights is a material failure of governance and internal control.

I request that you formally take this obstruction into account as part of your audit under the following specific provisions of the Local Audit and Accountability Act 2014:

Breach of Section 26(1) (Inspection of Documents): This section gives any interested person the absolute right to inspect the accounting records and all related documents. The Council’s deliberate delay and lack of response constitute a direct obstruction of this statutory right.

Failure Under Section 20(1)(c) (Value for Money & Governance): You have a statutory duty to satisfy yourself that the authority has made proper arrangements for securing economy, efficiency, and effectiveness in its use of resources. A breakdown in statutory compliance and public transparency directly undermines the Council’s governance framework.

Auditor Powers Under Schedule 7 (Public Interest Reports): You hold independent, absolute powers to issue a Public Interest Report regarding any matter coming to your attention during the audit. The Council’s wilful obstruction of public accountability is a matter of significant public interest that warrants formal reporting.

The guide you attached outlines my rights, but the Council is actively blocking them. As the external auditor, you are the independent safeguard. If a local authority can simply ignore electors until the inspection window closes, the statutory process is rendered meaningless.

Please confirm that this evidence of Wirral MBC’s non-compliance will be formally logged and evaluated as part of your assessment of their governance and Value for Money arrangements.

I initially requested access to the following documents on 9th July 2026:

The Income Ledgers: All ledger entries recording rental income, wayleave fees, or site-share revenue received by Wirral Council from telecommunications operators during the 2025/2026 financial year.

The Associated Contracts: Copies of the underlying lease agreements, pavement permits, or wayleave contracts corresponding directly to those 2025/2026 telecommunications income streams (protected as inspectable “contracts” and “deeds” under Section 26(1) of the Act).

The Insurance Expenditure Records: The Council’s active Corporate Public Liability Insurance policy schedule for the 2025/2026 financial year, alongside the specific ledger receipt/voucher confirming the premium payment made to the insurer.

The Accounts inspection window closes on 10th August 2026.

Please also note: as of today, this matter is with the press.

Yours sincerely,

| Paul Cardin about.me/paul.cardin |

26th July UPDATE

Six days later, and as Shaun Allen’s promised ‘end of July’ response date approaches, I’ve had no response at all to Email 4 from Michael Green at Wirral Council’s auditors Grant Thornton.

1st August UPDATE

As expected, I’ve received nothing from Shaun Allen (fin_publicinspection@wirral.gov.uk) despite him aiming to respond witth advice before the end of July 2026.

EMAIL 5

From: Paul Cardin

Date: Sat, 1 Aug 2026 at 09:30

Subject: Fwd: *corrected version* – FORMAL NOTICE OF INSPECTION: STATUTORY REQUEST FOR ACCOUNTS AND SUPPORTING RECORDS

To: <Fin_publicinspection@wirral.gov.uk>

Cc: <matthewbennett@wirral.gov.uk>, <danielkirwan@wirral.gov.uk>, Basnett, Paula (Councillor) <paulabasnett@wirral.gov.uk>

Dear Shaun Allen,

It’s 1st August 2026 and there is now a delay beyond the end of July.

Will you be aiming to advise me before the end of the accounts inspection window?

Best regards,

| Paul Cardin about.me/paul.cardin |

Response 3

24 days have now elapsed and I’ve got nowhere.

Here’s an email received on 3rd August 2026 from Shaun Allen of Wirral Council:

From: FIN_PublicInspection, <Fin_publicinspection@wirral.gov.uk>

Date: Mon, 3 Aug 2026 at 10:19

Subject: RE: *corrected version* – FORMAL NOTICE OF INSPECTION: STATUTORY REQUEST FOR ACCOUNTS AND SUPPORTING RECORDS

To: Paul Cardin, FIN_PublicInspection, <Fin_publicinspection@wirral.gov.uk>

Cc: matthewbennett@wirral.gov.uk <matthewbennett@wirral.gov.uk>, Kirwan, Daniel <danielkirwan@wirral.gov.uk>, Basnett, Paula (Councillor) <paulabasnett@wirral.gov.uk>

Dear Mr Cardin,

I apologise for the delay, I’m just waiting for clarification from a third party before sending the information, but yes we will certainly be responding before the closure of the inspection period.

Kind regards,

Shaun

Email 6

Email received from Wirral Council’s Shaun Allen on 5th August 2026:

From: FIN_PublicInspection, <Fin_publicinspection@wirral.gov.uk>

Date: Wed, 5 Aug 2026 at 09:29

Subject: RE: *corrected version* – FORMAL NOTICE OF INSPECTION: STATUTORY REQUEST FOR ACCOUNTS AND SUPPORTING RECORDS

To: Paul Cardin

Cc: Kirwan, Daniel <danielkirwan@wirral.gov.uk>, Bennett, Matthew <matthewbennett1@wirral.gov.uk>, Basnett, Paula (Councillor) <paulabasnett@wirral.gov.uk>, FIN_PublicInspection, <Fin_publicinspection@wirral.gov.uk>

Dear Mr Cardin,

Thank you again for your inspection request, and for subsequently setting out your concerns regarding access to the records requested during the public inspection period. I would like to reassure you that there is absolutely no intention on the Council’s part to block, delay unnecessarily, or otherwise deny your statutory rights of inspection. We fully recognise the importance of the public inspection process and the rights afforded to local electors under the relevant legislation.

The timescale previously indicated (31st July) was well within the public inspection period which concludes on 12th August, and reflects the practical work required to identify, collate, review and prepare the information requested. This involves liaising with a number of relevant officers, locating records, and ensuring that any information disclosed is accurate and appropriate for release. There has been a slight delay past the intended return date while we awaited third party confirmation.

Work has progressed as a priority, and I’m happy to attach the following:

1. Ledger transactions (telecoms / insurance);

2. Insurance schedule.

3. Insurance invoices and payments system screens confirming payment.

Unfortunately, I am unable to provide copies of lease agreements or contracts relating to the telecommunications income streams under sections 26 (4) (a) and 26 (5) (a) of the Local Audit and Accountability Act 2014, as these are protected on the grounds of commercial confidentiality.

Thank you for your patience and understanding while this work was undertaken.

Yours sincerely,

Shaun Allen

Senior Finance Manager

There were 6 attachments to the above email:

Wirral Council’s 2026 “NOTICE OF PUBLIC RIGHTS” document

(my emphasis / italics):

Wirral Metropolitan Borough Council

AUDIT OF ACCOUNTS YEAR ENDED 31ST MARCH 2026

NOTICE OF PUBLIC RIGHTS

The Accounts and Audit Regulations 2015

Local Audit and Accountability Act 2014

The Accounts and Audit (Amendment) Regulations 2024

Notice is hereby given under Regulation 15 (2 and 3) of the Accounts and Audit Regulations 2015 that the unaudited statement of accounts which may be subject to change for the year ended 31 March 2026 will be published on the Council’s website at: https://www.wirral.gov.uk/about-council/budget-and-spending/annual-accounts.

The period for the exercise of public rights under the Local Audit and Accountability Act 2014 and updated by The Accounts and Audit (Amendment) Regulations 2024,

is required to include the first 10 working days of July.

The accounts and other documents are available for inspection at Council’s offices at Wallasey Town Hall, Brighton Street, Wallasey, Wirral, CH44 8ED. Please email Shaun Allen at Fin_publicinspection@wirral.gov.uk to make an appointment.

Notice is given that from 1 July 2026 to 12 August 2026 (Inclusive) between 10:00 hours and 16:00 hours on weekdays any person may inspect the accounting records for the financial year to which the audit relates. The accounting records include all books, deeds, contracts, bills, vouchers, receipts and other related documents to those records and they may make copies of all or any part of those records or documents, as required under Section 25 of the Local Audit and Accountability Act 2014 (The Act), except as provided for in Section 26 of The Act.

Notice is given that from 1 July 2026 to 12 August 2026 (Inclusive) a local government elector for any area to which the accounts relate, or their representative, may ask the auditor questions about the accounts as set out in Section 26 of The Act.

Notice is given any such elector may make objections to the auditor, under Section 27 of The Act during this period, relating to any matter where the auditor could take action under:

• Section 28 of The Act, namely, to apply to the court for a declaration that an item in the accounts is contrary to law; and/or

• Section 24 and paragraph 1 of schedule 7 of The Act, namely, to make a report in the public interest.

Any objection, and the grounds on which it is made, must be sent to the auditor in writing, with a copy to Shaun Allen, Senior Finance Manager, at the following email address Fin_publicinspection@wirral.gov.uk. Any objection must state the grounds on which the objection is being made and particulars of the objection.

Objections should be directed to the auditor, Michael Green of Grant Thornton UK LLP (Landmark, St Peter’s Square, 1 Oxford Street, Manchester M1 4PB

(direct) +44 (0)161 953 6382 email michael.green@uk.gt.com).

• A guide to your rights can be found at: National Audit Office: Local authority accounts – a guide to your rights

30 June 2026

Daniel Kirwan

Interim Director of Finance (S151 Officer)

Wallasey Town Hall

Brighton Street

Wallasey

Wirral

CH44 8ED

danielkirwan@wirral.gov.uk

Return to Bomb Alley 1982 – The Falklands Deception, by Paul Cardin

Amazon link

{kind=link}

{kind=link}

John Brace left an annotation ()

Yes I’m following this one by email as of yesterday, as I have more info on it already. Next time I see Surjit Tour I’ll remind him.